Daniel Patrick Moynihan famously wrote, “Everyone is entitled to his own opinion, but not to his own facts.” In Washington, however, powerful interests frequently are entitled to their own facts—for the simple reason that they, and they alone, have access to them. When lawmakers and regulators sit down to write statutes or the rules to ensure that industries don’t cheat their customers, sully the environment, or (in the case of banks) put the whole economy at risk, the principal facts they have to work with are all too often chosen by the companies and industries themselves, from proprietary data sets they control.

Scientists at Exxon, for example, knew as far back as 1977 that man-made carbon emissions—such as those resulting from burning petroleum products—contribute to climate change. But instead of sharing this information with Congress or regulators, the company poured millions of dollars into phony climate-denial research and front groups. Likewise, tobacco companies knew as early as the 1950s about the dangers of smoking but chose to mount a multi-decade campaign of disinformation and obfuscation. And then there was the 2007 financial crisis, brought about by the activities of the “shadow-banking” system. Before the crisis, federal regulators had little information about the risky behaviors and positions of this sector and couldn’t have regulated it even if they had wanted to.

Sometimes the key information that public officials and citizens need to make informed decisions does emerge, but years after it would have been most helpful. It was a Pulitzer Prize–winning team of investigative reporters at the website Inside Climate News that exposed what Exxon knew and when it knew it. In the case of tobacco, a lawsuit brought by the U.S. Department of Justice under President Bill Clinton revealed the companies’ conspiracy.

But rather than wait for these occasional or serendipitous moments of revelation, the better course is for governments to have access to the same data industry has—at least to the extent that it bears on public policy and welfare. That was the lesson lawmakers took from the financial crisis when they drafted the Dodd-Frank financial reform legislation in 2010.

Dodd-Frank granted federal regulators broad access to what was once proprietary information held by financial institutions. For example, as part of the now-mandatory “stress tests” administered by the Federal Reserve, banks must disclose detailed data about their capital positions and risk management practices so regulators can assess their stability.

The law also created the Consumer Financial Protection Bureau (CFPB)—the first-ever federal agency aimed at regulating consumer financial products—and gave it expansive supervisory authority over not just banks but also non-bank financial institutions like mortgage brokers and payday lending outfits that had previously escaped serious scrutiny. Importantly, Congress gave the CFPB “examination” authority—that is, the power to demand the data necessary to carry out its mission of consumer protection—as well as the capacity to conduct independent research on any developments in the marketplace that could negatively affect consumers.

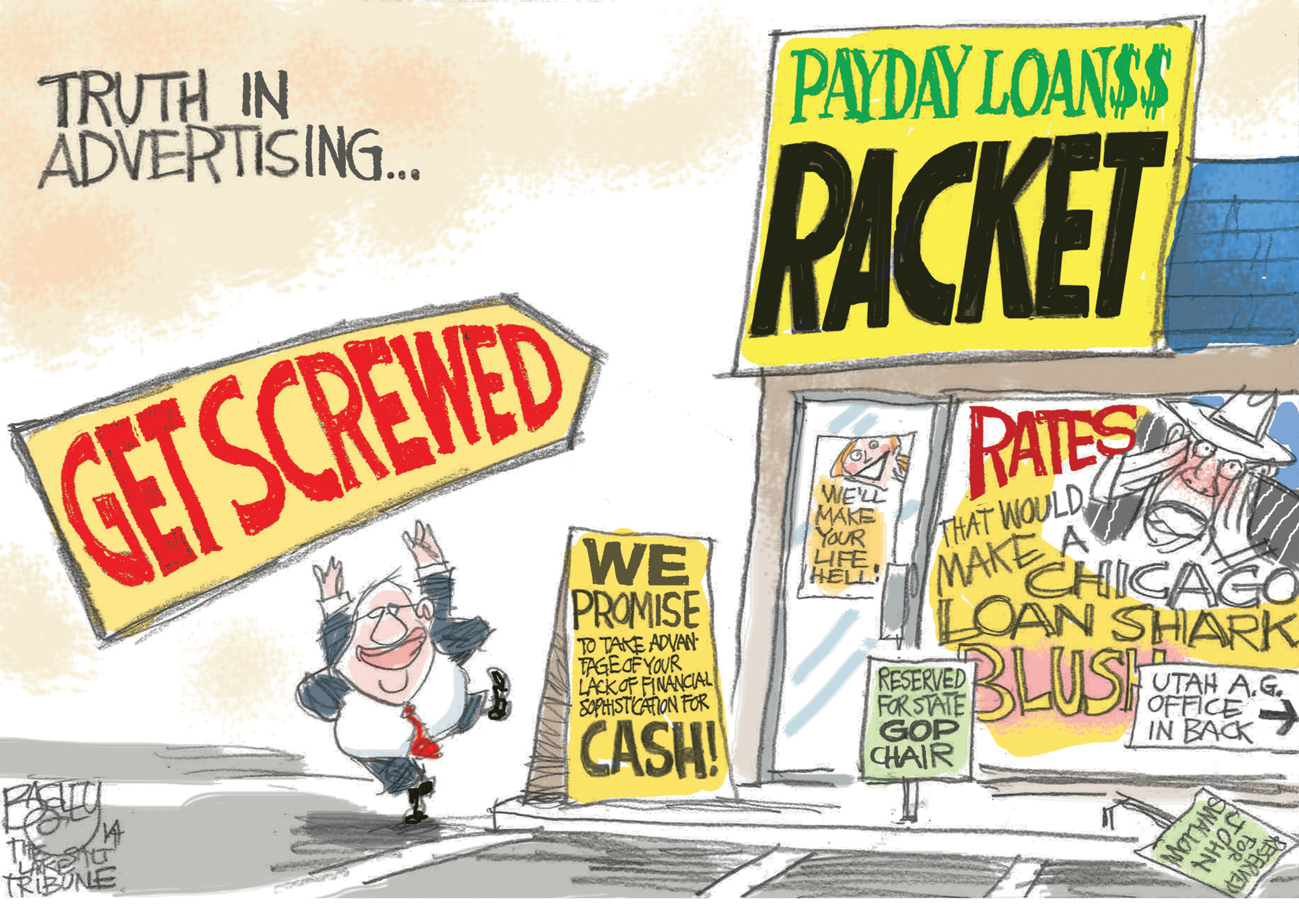

As the first exercise of its investigative and supervisory authority, the bureau in 2012 turned its sights on payday lending, an industry that had grown more or less unfettered for decades while preying on the nation’s most vulnerable customers. Its victims included people like Lisa Engelkins, who told the Center for Responsible Lending that she paid $1,254 in interest and fees on one $300 loan. As a single mom earning less than $8 an hour, she had the money to pay the fees but never enough to pay the principal, which she rolled over into new loans a total of thirty-five times. Another borrower, Sandra Harris, took out new payday loans to pay off old ones. She eventually held as many as six payday loans at the same time, paying $600 a month in fees alone.

To end these kinds of abuses, the CFPB announced in March 2015 its intent to regulate payday lending, along with a framework for what it might do. It is expected to propose and finalize new rules over the next year. Payday lenders are bracing themselves—the industry has all but stopped growing in anticipation—and a few state governments, emboldened by data dug up by the CFPB and several nonprofits, have started cracking down.

The battle over payday lending is far from over. The industry, with more than 20,600 storefronts nationwide and roughly $38 billion in annual revenue, has many powerful friends, on both sides of the aisle. Still, the story of how the CFPB broke the payday lending industry’s stranglehold on data is a valuable example of how government can regain leverage over industry actors who would impose their facts over the truth.

Governments have had laws against lending at high interest rates, or “usury,” since the Code of Hammurabi. At America’s founding, all thirteen original states had them. Over the nineteenth century, usury laws waxed and waned; many states repealed them, only to bring them back. By the turn of the twentieth century, the public had become concerned about the rise of illegally operated “salary lenders” offering short-term loans at high interest rates to desperate urban workers, often using brutal tactics and even violence to collect on their loans. Reformers argued that creating a carve-out for “small-dollar loans” would allow legitimate mainstream lenders, like banks and credit unions, to compete against illegal loan sharks while meeting the clear demand for short-term credit. In 1916, the American Bar Association helped develop model legislation for the regulation of these small loans—the Uniform Small Loan Law—which two-thirds of states ultimately adopted in some form. In those states, the annualized interest rates for small loans varied between 18 and 42 percent.

Things began to change in the 1980s, when banks, spurred by competitive pressures partly created by deregulation, stopped offering free checking accounts to customers who didn’t maintain minimum balances. To meet the needs of these largely low-income and suddenly unbanked individuals, check-cashing stores sprung up. Soon these stores started offering payday loans, too. In a typical payday loan transaction, borrowers write a postdated check that includes finance charges of $15 to $30 for every $100 borrowed, in exchange for immediate cash. The term of the loan is usually two weeks, which means these fees translate into an annualized interest rate of 400 percent or more.

Opponents argued that these practices violated state usury laws. Lenders maintained that they were providing a vital service banks had abandoned. State legislators responded by giving payday lenders exemptions from usury laws and allowing them to charge triple-digit interest rates. (Substantial campaign contributions from payday lenders also greased the way for these decisions.) By 1999, according to the Consumer Federation of America (CFA), twenty-three states and the District of Columbia had carved out safe harbors for payday lending, while another seven states had no caps on interest rates.

Now facing friendly terrain, the payday industry exploded, growing from just a few hundred stores in the 1990s to more than 24,000 outlets by 2007. By 2008, according to one study, payday lending outlets outnumbered all Starbucks and McDonald’s stores combined.

As the payday lending industry mushroomed, consumer advocates began to collect a growing number of horror stories from borrowers—people like Lisa Engelkins and Sandra Harris—who were caught in an endless cycle of debt. Yet the lack of real data about the industry’s practices made it difficult for reform advocates to make headway, either federally or in the states. For example, a 1998 report from the CFA noted that despite the industry’s exponential growth, “[p]ublic data on the profitability of payday lending is sketchy.” And crucially, advocates didn’t have the data to counter one of the industry’s central claims: that payday loans served as an occasional source of emergency funding to tide people over in a pinch. According to the industry, repeat borrowers like Engelkins and Harris were very much the exception, not the rule.

“[The industry would say,] ‘Look, these are very poor people, they have no access to credit, no access to emergency loans, and you’re going to leave them even worse off if you undercut us,’ ” says New Mexico state representative Javier Martínez, who also serves as the executive director of the Partnership for Community Action. “And oftentimes proponents of reform were unable to respond in a direct substantial way,” Martínez says. By the mid-2000s, the states that regulated payday lending were beginning to collect more data, which made more and better research possible. In 2005, for example, the Center for Responsible Lending (CRL) published a study showing the abnormally high concentration of payday lenders in military towns and in African American communities in North Carolina.

The industry fought back with a clever strategy: pay “independent” researchers to do counter studies using the industry’s own (uncheckable) data. The first of these reports appeared in 2005, when a researcher funded by the Consumer Credit Research Foundation (CCRF), an industry-affiliated nonprofit, published a study concluding that taking out a payday loan was less costly than bouncing a check. In 2006, the same researcher, Thomas Lehman, published a critique of the CRL’s study of North Carolina.

Other studies published during the latter half of the 2000s touted the economic benefits payday lending brought to communities and the satisfaction of its customers while at the same time reinforcing perceptions of the product as a short-term solution for Americans facing an unexpected financial crisis. One CCRF-funded study, for example, authored by Jonathan Zinman of Dartmouth College in 2008, argued that when the availability of payday loans in Oregon diminished after its regulation, consumers turned to “plausibly inferior substitutes” such as running overdrafts.

“[These claims] were pretty successful where policymakers were not on board with payday lending as a good product but thought it provided a service banks weren’t providing,” says David Rothstein, the director of resource development and public affairs at Neighborhood Housing Services of Greater Cleveland. Moreover, he says, state legislators who prided themselves as “pro-growth” were reluctant to shut down an industry arguably circulating dollars in the economy.

Not surprisingly, the industry was not inclined to share its data with other researchers. Professor James Barth, the Lowder Eminent Scholar in Finance at Auburn University, says he hit a “dead end” when he asked payday lending companies for data several years ago. “I tried a couple of times,” Barth says. “I never got a ‘no,’ but after a couple attempts, I never heard anything.”

In fact, the industry has gone to great lengths—such as through litigation—to keep its data secret. When Alabama legalized payday lending in 2003, it set a $500 maximum on what customers could borrow at any given time. When the state’s banking department tried to create a payday loan database to keep track of these loans, the industry sued to block it. “They wanted to selectively deploy information as it suits their needs as opposed to having state-sanctioned data about their business,” says Stephen Stetson, a policy analyst at the nonprofit advocacy group Alabama Arise.

As the industry grew exponentially throughout the 1990s and into the 2000s and consumer complaints began to mount, reformers made some headway. In 2007, Congress banned payday lending to military personnel and their families. In 2008, Ohio passed legislation capping payday loan interest rates at 28 percent, and in 2009, New Hampshire capped interest rates at 36 percent. Montana and Colorado followed suit in 2010.

These were scattered victories, though; the real reform action was still to come. In 2011, the CFPB began building out its Office of Research. In January 2012, it conducted its first field hearing on payday lending, in Birmingham, Alabama, where CFPB director Richard Cordray announced the publication of a field guide for agency examiners who would be deployed across the country to study payday lending practices firsthand. In June 2012, the agency established a portal for consumers to file complaints and created a searchable database for the complaints it received.

During these initial years, the CFPB’s future was far from assured. Congressional Republicans made no secret of their hatred of the agency and repeatedly tried to weaken its independence. Senator Ted Cruz introduced legislation to kill it off. In this uncertain environment, major philanthropically supported nonprofits stepped forward to conduct their own research. In 2012, the Pew Charitable Trusts released the first of a series of reports based on extensive surveys of payday loan borrowers—surveys that, in effect, mirrored the proprietary data independent researchers couldn’t get the industry to share. The report mounted a frontal assault against the industry’s claims that payday loans are an emergency product: “Payday loans are often characterized as short-term solutions for unexpected expenses, like a car repair or emergency medical need. However, an average borrower uses eight loans lasting 18 days each, and thus has a payday loan out for five months of the year.”

In 2013, Pew followed up its initial study with another report that further undermined the industry’s argument of payday lending as a short-term fix and undercut the industry’s arguments of customer “satisfaction” by finding that many borrowers opted for payday loans out of “unrealistic expectations and by desperation.” Similar findings also emerged from a 2012 survey of payday borrowers by the Center for Financial Services Innovation, published with the support of the Ford Foundation.

In April 2013, the CFPB’s Office of Research issued its first white paper on payday lending, based on its analysis of twelve million loans from thirty states over a twelve-month period from 2011 to 2012. This report was followed by a second study in March 2014. The research conclusively shattered some of the industry’s key claims—using industry data. In particular, it demolished the industry’s denial of the “debt trap” created by its products. “[T]he core payday loan product was designed and justified as being expressly intended for short-term emergency use,” said Cordray in 2014 at the release of the CFPB’s report. “But our study today again confirms that payday loans are leading many consumers into longer-term, expensive debt burdens.” For example, the CFPB said, as many as 48 percent of payday loan borrowers had taken out ten or more loans over a twelve-month period, and more than four in five loans were being renewed within fourteen days of origination.

For proponents of reform, the results of the CFPB’s research represented both the vindication they had sought for years and the weapon they needed for victory. “It’s the fuel for how we’re going to be able to drive reform at the federal and state levels,” says advocate David Rothstein.

In one telling sign of the shift that’s taken place, the industry appears to have stopped arguing that payday loans are an emergency, lifeline product. In 2012, Dennis Shaul, CEO of the industry’s largest trade association, the Community Financial Services Association of America, had testified before the U.S. Senate that “[p]ayday loans are one option for those who need help to make it to the next paycheck.” But in February 2016, this time testifying before a House committee, Shaul changed his tune: “Payday loans, perhaps once used more often to meet emergency expenses, are now used to offset income disruptions as well,” he testified.

“The reality of the debt trap is indisputable,” says Tom Feltner, the Consumer Federation of America’s director of financial services. “The debate has changed from whether or not intervention is needed to what type of intervention is the most helpful.”

Among the benefits of the CFPB’s research-driven approach to regulation is that it provides a credible evidentiary foundation for its eventual rule making—a must if the rules are to survive the challenges the payday lending industry will undoubtedly bring, both in the courts and by their allies in Congress. The proposed regulatory framework the agency announced in March 2015 includes “debt trap prevention” requirements such as a limit on the number of loans a borrower can take out in one year and consideration of a borrower’s ability to repay before lenders can make or renew a loan. Both proposals are squarely aimed at ending the cycle of repeated borrowings that the CFPB found in its data.

More so than even campaign contributions, information imbalances give powerful interests the leverage to turn policymaking in Washington to their advantage. But in the case of payday lending, regulators were able to crack the vault–and consumers will see the benefits.

The CFPB’s research has also had important spillover effects on reform efforts in the states. “The joint federal and state jurisdiction over payday lending is going to be the tipping point for states,” Feltner says. In Alabama, for example, state legislators are currently contemplating two separate payday lending reform bills, one of which passed the state senate 28–1 in April. “We have a much different environment this year than in years past,” says Arthur Orr, the Republican state senator who was the bill’s sponsor.

Republican State Representative Danny Garrett, the sponsor of the other payday loan reform bill pending in the state, says the availability of both state and national data has been a major factor in the momentum for reform. Last year, the Alabama Supreme Court ruled against the payday lenders who sued to keep their data private, and in August 2015 the state’s payday loan database became operational.

“People are realizing that this product is preying upon a small proportion of the population and generating huge revenue at a huge profit,” Garrett says. “In years past, the industry could always talk about this wonderful service they provided to all these people. They can’t say that anymore. We have data that shows what it is.”

There are three lessons to be drawn from this story. First, lawmakers should empower more agencies of government with the authority and budgets to do what the CFPB has done. From regulating telecommunications to contracting out services, government agencies are perpetually at a disadvantage because of asymmetries of information between themselves and the private entities they are charged with overseeing. It is these information imbalances, more so than things like campaign contributions, that give powerful interests the leverage to turn policymaking in Washington to their advantage.

Second, Congress should empower itself to gather more of its own information and expand its capacity to interpret the data it receives from external sources. As this magazine has argued (Paul Glastris and Haley Sweetland Edwards, “The Big Lobotomy,” June/July/August 2014), Congress twenty-five years ago gutted, through staff and budget cuts, much of the internal research ability it once possessed. Today, members have little in the way of in-house expertise to referee competing and polarizing claims on such contentious issues as climate change, the impact of trade agreements, gun control and gun violence, and the likely effects of raising the minimum wage. This lack of research capacity is especially alarming when it comes to emerging issues where disruptions in technology and business have opened up a regulatory vacuum, such as the oversight of the “on-demand” economy. Despite the angst among many policymakers about the “Uberization” of the modern workforce, Congress currently lacks even the most basic information about this trend—how many on-demand workers are there, for example, and what are their economic circumstances?

Third, to the extent Congress can’t or won’t execute these two tasks itself, there is a potentially vital role that the non-profit and philanthropic community can play in investing in independent research and helping policymakers challenge the one-sided narrative they might hear from industry.

A foundation of the American legal system is that each side in a lawsuit must have access to the same evidence base—indeed, if one side is caught withholding such evidence, it can be grounds for the other side to have the case thrown out or overturned. Yet for some reason, we do not apply this obviously sensible rule to policymaking. Simply giving government the authority to see the same data that industry lobbyists possess would go a long way toward making Moynihan’s memorable maxim about the role of facts actually true in Washington.